The Financial Reform

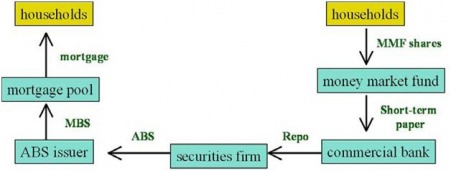

Before addressing the different reform proposals, we offer a simple view of the situation in the securities markets. Before the crisis, conventional wisdom thought that securities and financial innovations distributed risk to those best able to bear it. This is how complicated the financial sector looked during the bubble:

Such a system created a misalignment of incentives that resulted in excessively risky investments. The financial reform should address the misalignment.

The Obama Proposal

The Obama administration has been trying to pass a financial reform since 2009. Initially longer than 4,000 pages, the latest version of the proposal has been slimmed down to 1,336 pages. The bill is under the responsibility of the Senate Banking Committee, which has members from both the Democrat and the Republican parties, and is led by Connecticut Democrat Christopher J. Dodd (with support from Treasury Secretary timothy Geithner).

At first, the proposal included the creation of a Consumer Financial Protection Agency (CFPA), but Republicans rejected this idea on the basis that they did not want another layer of bureaucracy added to the government. Instead, the agency will be created as a part of the Fed.

The director would be appointed by the president and confirmed by the Senate. The agency would be an independent entity in the Federal Reserve with a separate budget but not reporting to theFed. An agency decision could be vetoed by a two-thirds vote of a new council of financial regulators (LA Times, March 16, 2010), the Financial Services Oversight Council (FSOC). The FSOC would be formed by members of the Fed, the Treasury, the National Bank Supervisor, the SEC, the FDIC, the CFTC and the director of the CFPA.

The CFPA will have the power to oversee the financial sector, look for systemic risk and even intervene in large institutions crucial to the economy. Other important aspects of the bill are to increase capital requirements, close loopholes in bank regulation (which would reduce intermediaries), require hedge funds to register, determine the future role of government-sponsored entities such as Fannie Mae and Freddie Mac, and other general regulatory overhauls. Also, it would require large foreign banks to adhere to the same regulations as large U.S. banks that are considered crucial.

At first, the proposal included the creation of a Consumer Financial Protection Agency (CFPA), but Republicans rejected this idea on the basis that they did not want another layer of bureaucracy added to the government. Instead, the agency will be created as a part of the Fed.

The director would be appointed by the president and confirmed by the Senate. The agency would be an independent entity in the Federal Reserve with a separate budget but not reporting to theFed. An agency decision could be vetoed by a two-thirds vote of a new council of financial regulators (LA Times, March 16, 2010), the Financial Services Oversight Council (FSOC). The FSOC would be formed by members of the Fed, the Treasury, the National Bank Supervisor, the SEC, the FDIC, the CFTC and the director of the CFPA.

The CFPA will have the power to oversee the financial sector, look for systemic risk and even intervene in large institutions crucial to the economy. Other important aspects of the bill are to increase capital requirements, close loopholes in bank regulation (which would reduce intermediaries), require hedge funds to register, determine the future role of government-sponsored entities such as Fannie Mae and Freddie Mac, and other general regulatory overhauls. Also, it would require large foreign banks to adhere to the same regulations as large U.S. banks that are considered crucial.

Glass-Steagall and The Volcker Rule

Republican Senator John McCain and Democrat Senator Maria Campbell jointly proposed to re-enact Glass-Steagall in December of 2009. While the proposal did not succeed, the Volcker rule contains many of the important aspects of Glass Steagall. By limiting certain types of trades, the Volcker rule achieves similar results to separating commercial and investment banking.

Former Federal Reserve Chairman Paul Volcker argues for restricting certain kind of speculative investments by banks if they are not in behalf of their clients. The logic behind the argument is to make clients hold banks accountable for their money, rather than allow banks to invest freely and endangering the patrimony of clients. Volcker's proposal specifically prohibits banks from propietary trading (trading in stocks, derivatives, etc.) unless it is on behalf of their clients. When banks trade their own money, their employees have incentives to take high risks because they can get high rewards without bearing any risk. The Volcker rule would correct this misalignment of incentives. However, the current financial reform bill does not include the Volcker rule. Instead, an independent authority would determine which activities are considered too risky for banks to take.

Republican Senator John McCain and Democrat Senator Maria Campbell jointly proposed to re-enact Glass-Steagall in December of 2009. While the proposal did not succeed, the Volcker rule contains many of the important aspects of Glass Steagall. By limiting certain types of trades, the Volcker rule achieves similar results to separating commercial and investment banking.

Former Federal Reserve Chairman Paul Volcker argues for restricting certain kind of speculative investments by banks if they are not in behalf of their clients. The logic behind the argument is to make clients hold banks accountable for their money, rather than allow banks to invest freely and endangering the patrimony of clients. Volcker's proposal specifically prohibits banks from propietary trading (trading in stocks, derivatives, etc.) unless it is on behalf of their clients. When banks trade their own money, their employees have incentives to take high risks because they can get high rewards without bearing any risk. The Volcker rule would correct this misalignment of incentives. However, the current financial reform bill does not include the Volcker rule. Instead, an independent authority would determine which activities are considered too risky for banks to take.

Republican Senator John McCain and Democrat Senator Maria Campbell jointly proposed to re-enact Glass-Steagall in December of 2009. While the proposal did not succeed, the Volcker rule contains many of the important aspects of Glass Steagall. By limiting certain types of trades, the Volcker rule achieves similar results to separating commercial and investment banking.

International Financial Reform Agenda

The members of the G-20 agreed to create the Financial Stability Board (FSB), which would enforce an international financial reform. The FSB would increase capital requirements, would demand countercyclical buffers, and would check on leverage ratios. It is difficult to understand how this new institution‘s goals will differ from that of the Obama proposal because the web versions available are just summaries of the documents. However, some of the implications are that many countries will have to increase regulation in the banking sector. Others, like Spain, will remain practically unaffected. By checking capital requirements, leverage ratios and countercyclical buffers, the FSB can prevent future financial crises. High capital requirements and leverage ratios will force banks to have more assets and less liabilities in their balance sheets, and hence will reduce the risk of banks going bankrupt due to shortages of capital, failed investments, etc..

Will the reform be effective?

The CFPA will have the authority to prohibit propietary trades, which is like enforcing the Volcker Rule. Such authority would have been sufficient to prevent the housing bubble, but the true answer lies in the details. Had it existed, would the CFPA have used its authority to prohibit propietary trades? Almost nobody knew the extent of the housing bubble and it is doubtful the CFPA would have noticed either, so it is not a matter of authority, but a matter of how well the CFPA can monitor the market. Furthermore, it is a matter of how well can the CFPA resist lobbies from the financial sector. However, future financial bubbles are likely to be well-monitored because (hopefully) regulators will have learned from past policy mistakes.

Another problem associated with the CFPA is the extent of its authority. Too much power in one agency means that if it is not well managed, costly mistakes can happen. Therefore, the FSOC will have the power to veto CFPA decisions. That veto power is a problem too: too much disagreement amongst the varied membership of the FSOC could handcuff the CFPA. Yet, systems with checks and balances have worked pretty well for the U.S. government, and really the alternatives are probably much worse.

The reform is increasing regulation in the financial sector significantly. Shadow banking will be no more as banks and funds will have to report everything to the SEC or the CFPA. However, a big part of the new regulation is focused on large banks because these can have a systemic impact if they fail. Focusing regulation on large banks can incentive the fragmentation of the financial sector, which could lead to a scenario of small, not-so-regulated banks and no large banks. Having a lot of small underregulated banks would make it very hard for any agency to monitor systemic risk, and therefore would make another financial crisis likely.

Overall, the financial reform does a good job at addressing the misalignments of incentives. The CFPA will monitor these with some flexiblity rather than with a rule. However, the unintended consequences of the bill could be enormous.

Another problem associated with the CFPA is the extent of its authority. Too much power in one agency means that if it is not well managed, costly mistakes can happen. Therefore, the FSOC will have the power to veto CFPA decisions. That veto power is a problem too: too much disagreement amongst the varied membership of the FSOC could handcuff the CFPA. Yet, systems with checks and balances have worked pretty well for the U.S. government, and really the alternatives are probably much worse.

The reform is increasing regulation in the financial sector significantly. Shadow banking will be no more as banks and funds will have to report everything to the SEC or the CFPA. However, a big part of the new regulation is focused on large banks because these can have a systemic impact if they fail. Focusing regulation on large banks can incentive the fragmentation of the financial sector, which could lead to a scenario of small, not-so-regulated banks and no large banks. Having a lot of small underregulated banks would make it very hard for any agency to monitor systemic risk, and therefore would make another financial crisis likely.

Overall, the financial reform does a good job at addressing the misalignments of incentives. The CFPA will monitor these with some flexiblity rather than with a rule. However, the unintended consequences of the bill could be enormous.